The budget is where we start our “number crunching” for the year. There are multiple parts to our budget – a budget for each enterprise (beef, pork and chicken in our case) and an overall budget for the farm as a whole.

[Of course let me throw out the disclaimer that this is what works for us. This is by no means professional advice. I’m looking forward to hearing how some of you budget, so that we can continue to evolve our own process.]

Okay, so the enterprise budgets include only the income and expenses directly related to the enterprise.

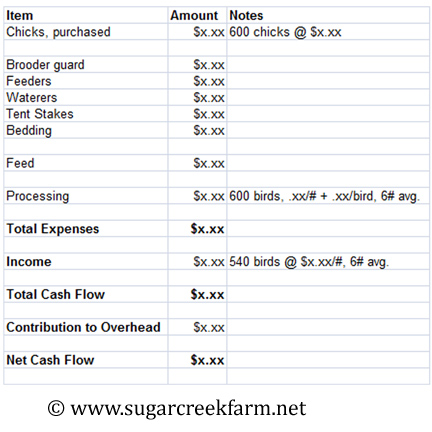

As you can see from our broilers budget spreadsheet, it’s pretty simple and straightforward. The expenses basically follow the life cycle of the birds. You’ve got the cost of purchasing the chicks, supplies for brooding and finishing, feed, and finally processing.

Similarly, the beef budget includes expense items such as vet work (castration), the rent we pay for our hay ground, hired labor to make cut & bale the hay and cornstalks, and tractor expense because the tractor is used 95% of the time for beef-related tasks.

In order to be conservative, I budget feed and expenses for the full batch of 600 chicks. But for estimating sales & income I assume a 10% death loss, so out of 600 chicks I figure on ending up with 540 birds at butchering time.

With chickens income is simple to figure:

(average weight of your dressed bird) x (price per lb.) x (number of birds)

Or perhaps you’re charging a flat price per bird (though I’ll warn you there are labeling issues with this that you have to be careful with.) Then of course it’s just (price) x (# of birds).

When it comes to beef & pork things are more complicated – we have on-the-hoof, wholesale, and retail sales. In a nutshell we project how many head we’re going to sell in each category, for what price, and add up to a total income. In reality this is more complicated than that sentence sounded! I’ll save the details for another post – if I can even manage to explain how we work our crystal ball!

Note that these are cash expenses. So things like depreciation are not included here. Depreciation is a non-cash expense that comes into play later on in the Profit & Loss.

See the category “Contribution to Overhead”? This is the amount that this particular enterprise is going to contribute to the general expenses of the farm as a whole – insurance, taxes, advertising, etc. More on that in the next installment in this series.

Even though we budget a year at a time, you certainly don’t have to. The main reason we do it this way is that we send out one newsletter early in the year with our prices for the year in it. Depending on how you do things on your farm, and what enterprises you have, it might make more sense for you to budget over a shorter or longer timespan.

The thing about budgeting is that it’s most difficult the first year, when you have no historical data to go on. So sometimes you just have to put out your best guess. Make some notes to yourself right with your budget about what assumptions you made to arrive at that guess. You’ll reap the benefits of it next year when you go to do your second budget. You’ll be able to see which assumptions were right and which were wrong so that you can make corrections.

So, do you budget? I’m guessing that there are as many ways of budgeting as there are farms. How do you budget?

Very interesting, thanks.